Are electric vehicles a technology for the rich?

This has definitely been the prevailing perspective so far. But it is actually three perspectives clubbed together, and in these interesting times of rapid change, this framing is worth a closer look.

The framing of EVs as a technology for the rich, when expanded, implies:

- EVs are expensive and out of affordable reach of all but the small minority of vehicle owners.

- EV technology (especially manufacturing) is controlled by wealthy industrialised economies and will remain so.

- At its core, private vehicle ownership is unsustainable in material and energy use – a lifestyle accessible only for the wealthy few. EVs lessen the impact, but the world does not have the resources for everyone to own a car.

Let’s examine these statements one by one:

1) EVs are expensive and out of affordable reach of all but the small minority of vehicle owners.

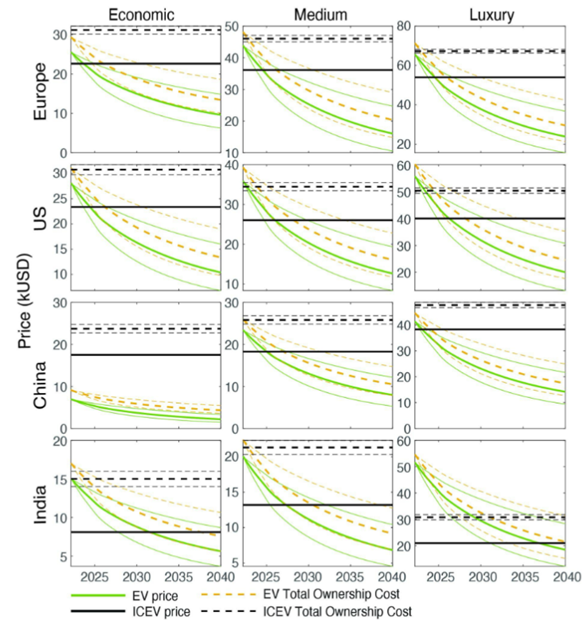

Figure 1, from a recent Nature article1, authored among others by the Wold Bank, looks at the the total cost of ownership (TCO) and purchase price of EVs and ICEs around the world. The data covers economic, medium and luxury vehicle sectors in the world’s largest automobile markets: the EU, US, China and India.

In China, both purchase price and TCO are already on par or lower than ICEV costs in economic, medium and luxury vehicles. A similar shift is expected to occur in the EU and US well before 2030 and in India around 2030. This shift is not just in the TCO, but also in the purchase cost of vehicles – often seen as the single biggest obstacle to mass EV adoption!

In fact, if China is to be taken as an example, the largest cost savings are in the economic car category, and it is that segment that EVs will have most financial appeal.

So although, EVs were definitely expensive in the past, particularly in terms of purchase cost, that will likely not be true for much longer a major global markets. In fact, they may make car transportation more economic overall.

2) EV technology (especially manufacturing) is controlled by wealthy industrialised economies, and will remain so.

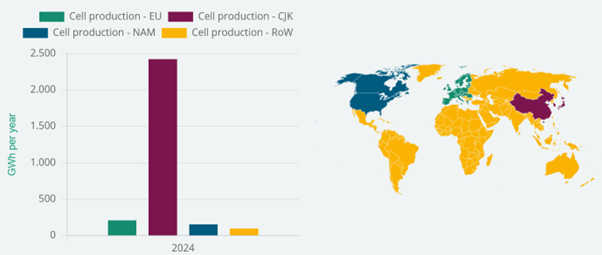

It is unquestionably clear that EV technology – or to be more precise, battery cell manufacturing is controlled by a few countries. Fraunhofer’s Institute’s global map from 20242 shown below in reveals how China, Japan and Korea (CJK) vastly outcompete North America (NAM), the EU and the rest of the World (RoW) in cell manufacturing.

This shows that technical capacity is unequally spread even amongst industrialised nations. It is a few Asian giants rather than industrialised nations that dominate manufacturing.

Globally, less than 5% of passenger vehicles are EVs (based on IEA estimates). Though individual countries are racing ahead, it is still the stage of the earliest of early adopters in terms of technology adoption at the global level. Other countries are expected to rapidly imitate or replicate the fastest movers, both in manufacturing and adoption. Both the US and Europe have plans to expand manufacturing capacity to around 1,500 GWh each by 2030, and others no doubt have similar plans.

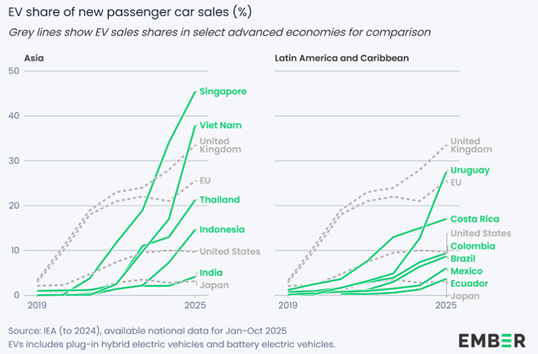

It is in market adoption, rather than manufacturing, that the shift to electrify is most rapid, seen in Figure 3, taken from Ember’s 2025 report on EV leapfrogging – how emerging markets are rapidly electrifying3. Singapore, Vietnam , Thailand, Uruguay and Costa Rica are electrifying extremely fast.

Though these economies are not yet producing battery cells, local automobile manufacturers like Togg in Türkiye, Vinfast in Vietnam and TVS Motors and Bajaj in India (for two wheelers) are often the companies with leading market share. With strong local market players, localization of cell production, shortening of supply chains and economizing of material use are likely to continue with market consolidation.

Thus, while battery cell production remains a under the control of the Asian giants, markets have moved much faster. We see emerging markets rapidly electrifying with high market shares of local players, and cell production is likely to follow the market.

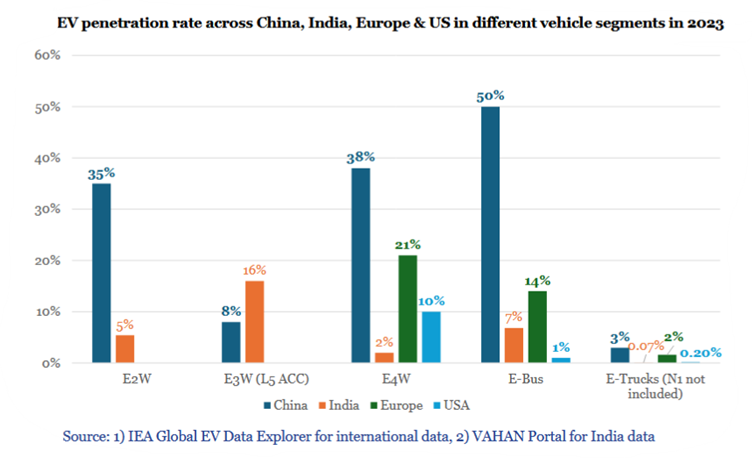

3) At its core, private vehicle ownership is unsustainable in material and energy use – a lifestyle accessible only for the wealthy few. EVs lessen the impact, but the world does not have the resources for everyone to own a car.

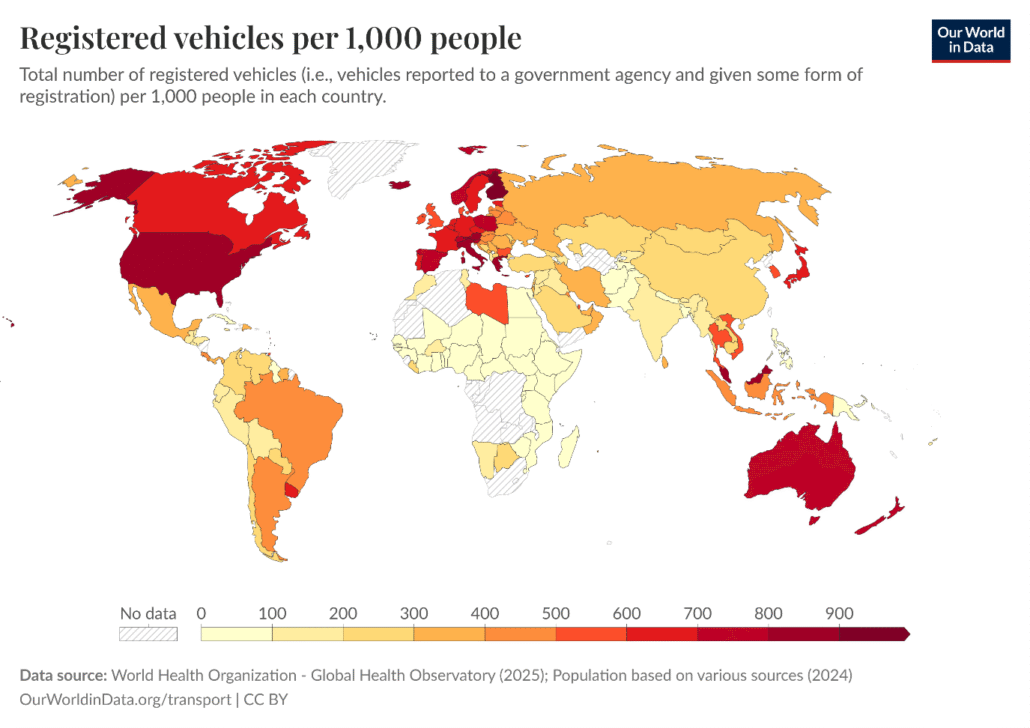

It is definitely true that the world does not have enough resources for globalized adoption of the vehicle ownership rates of industrialised nations (typically over 600 vehicles per 1000 people, as shown below)

However, as Figure 5 below shows, this is no barrier to electrification. India, the world’s largest market for 2 and 3 wheelers is rapidly electrifying those segments, with far lower cost and material use. Similarly, it seems likely that different countries will adapt electrification technologies for application in local contexts within existing resource constraints.

In conclusion, it is likely that vehicle electrification will make broad impact with price advantage across the entire range of customers from budget vehicles to luxury vehicles. While manufacturing capabilities related to battery technologies are currently limited to a very small group (China, Japan and South Korea), markets across the globe are rapidly transforming. As markets grow and consolidate, manufacturing is likely to spread as well. Vehicle segments are electrifying differently, and likely the pathway to prosperity will have different resource and carbon impacts.

-Rishabh Ghotge and Shiva Noori

- J.-F. Mercure, A. Lam, J. E. Buxton, C. A. Boulton, A. Akther, and T. M. Lenton, ‘Evidence of a cascading positive tipping point towards electric vehicles’, Nat Commun, vol. 17, no. 1, p. 240, Dec. 2025, doi: 10.1038/s41467-025-66945-9. ↩︎

- Fraunhofer ISI, ‘Cell Production – World map – MetaMarktMonitoring’. Accessed: Feb. 13, 2026. [Online]. Available: https://metamarketmonitoring.de/en/cell-production/worldmap.php ↩︎

- ‘The EV leapfrog – how emerging markets are driving a global EV boom’. Accessed: Feb. 13, 2026. [Online]. Available: https://ember-energy.org/app/uploads/2025/12/The-EV-leapfrog-PDF.pdf ↩︎